Doomsday clock for global market crash strikes one minute to midnight as central banks lose control

China currency devaluation signals endgame leaving equity markets free to collapse under the weight of impossible expectations

It is only a matter of time before stock markets collapse under the weight of their lofty expectations and record valuations. Photo: Reuters

By John Ficenec 8:00PM BST 16 Aug 2015

When the banking crisis crippled global markets seven years ago, central bankers stepped in as lenders of last resort. Profligate private-sector loans were moved on to the public-sector balance sheet and vast money-printing gave the global economy room to heal.

Time is now rapidly running out. From China to Brazil, the central banks have lost control and at the same time the global economy is grinding to a halt. It is only a matter of time before stock markets collapse under the weight of their lofty expectations and record valuations.

The FTSE 100 has now erased its gains for the year, but there are signs things could get a whole lot worse.

1 – China slowdown

China was the great saviour of the world economy in 2008. The launching of an unprecedented stimulus package sparked an infrastructure investment boom. The voracious demand for commodities to fuel its construction boom dragged along oil- and resource-rich emerging markets.

• Ambrose Evans-Pritchard: China cannot risk the global chaos of currency devaluation

The Chinese economy has now hit a brick wall. Economic growth has dipped below 7pc for the first time in a quarter of a century, according to official data. That probably means the real economy is far weaker.

The People’s Bank of China has pursued several measures to boost the flagging economy. The rate of borrowing has been slashed during the past 12 months from 6pc to 4.85pc. Opting to devalue the currency was a last resort and signalled the great era of Chinese growth is rapidly approaching its endgame.

Data for exports showed an 8.9pc slump in July from the same period a year before. Analysts expected exports to fall only 0.3pc, so this was a huge miss.

The Chinese housing market is also in a perilous state. House prices have fallen sharply after decades of steady growth. For the millions who stored their wealth in property, it makes for unsettling times.

2 – Commodity collapse

The China slowdown has sent shock waves through commodity markets. The Bloomberg Global Commodity index, which tracks the prices of 22 commodity prices, fell to levels last seen at the beginning of this century.

The oil price is the purest barometer of world growth as it is the fuel that drives nearly all industry and production around the globe.

• Andrew Critchlow: Oil companies travel back to 1986 in search of a future

Brent crude, the global benchmark for oil, has begun falling once again after a brief rally earlier in the year. It is now hovering above multi-year lows at about $50 per barrel.

Iron ore is an essential raw material needed to feed China’s steel mills, and as such is a good gauge of the construction boom.

The benchmark iron ore price has fallen to $56 per tonne, less than half its $140 per tonne level in January 2014.

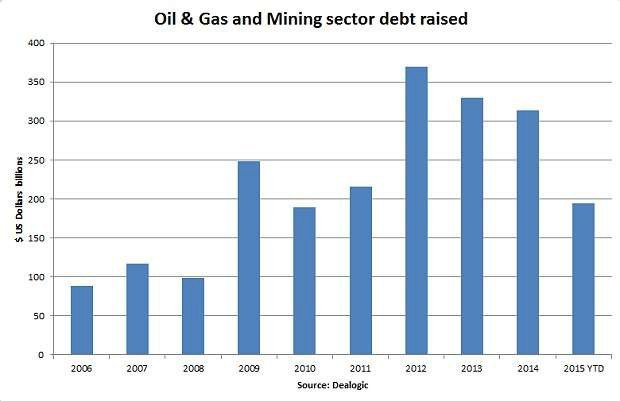

3 – Resource sector credit crisis

Billions of dollars in loans were raised on global capital markets to fund new mines and oil exploration that was only ever profitable at previous elevated prices.

With oil and metals prices having collapsed, many of these projects are now loss-making. The loans raised to back the projects are now under water and investors may never see any returns.

Nowhere has this been felt more acutely than shale oil and gas drilling in the US. Tumbling oil prices have squeezed the finances of US drillers. Two of the biggest issuers of junk bonds in the past five years, Chesapeake and California Resources, have seen the value of their bonds tumble as panic grips capital markets.

As more debt needs refinancing in future years, there is a risk the contagion will spread rapidly.

4 – Dominoes begin to fall

The great props to the world economy are now beginning to fall. China is going into reverse. And the emerging markets that consumed so many of our products are crippled by currency devaluation. The famed Brics of Brazil, Russia, India, China and South Africa, to whom the West was supposed to pass on the torch of economic growth, are in varying states of disarray.

• Is the global economy headed for another crash? Three signs to watch out for

- Regulators could be responsible for next financial crash

- Global stock markets jolted by China’s historic renminbi devaluation

The central banks are rapidly losing control. The Chinese stock market has already crashed and disaster was only averted by the government buying billions of shares. Stock markets in Greece are in turmoil as the economy grinds to a halt and the country flirts with ejection from the eurozone.

Earlier this year, investors flocked to the safe-haven currency of the Swiss franc but as a €1.1 trillion quantitative easing programme devalued the euro, the Swiss central bank was forced to abandon its four-year peg to the euro.

5 – Credit markets roll over

As central banks run out of silver bullets then, credit markets are desperately seeking to reprice risk. The London Interbank Offered Rate (Libor), a guide to how worried UK banks are about lending to each other, has been steadily rising during the past 12 months. Part of this process is a healthy return to normal pricing of risk after six years of extraordinary monetary stimulus. However, as the essential transmission systems of lending between banks begin to take the strain, it is quite possible that six years of reliance on central banks for funds has left the credit system unable to cope.

Credit investors are often far better at pricing risk than optimistic equity investors. In the US while the S&P 500 (orange line) continues to soar, the high yield debt market has already begun to fall sharply (white line).

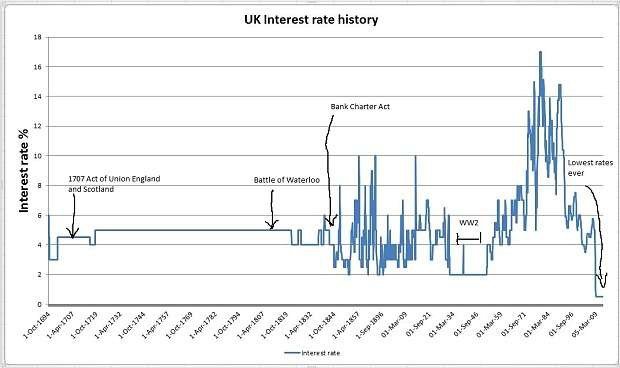

6 – Interest rate shock

Interest rates have been held at emergency lows in the UK and US for around six years. The US is expected to move first, with rates starting to rise from today’s 0pc-0.25pc around the end of the year. Investors have already starting buying dollars in anticipation of a strengthening US currency. UK rate rises are expected to follow shortly after.

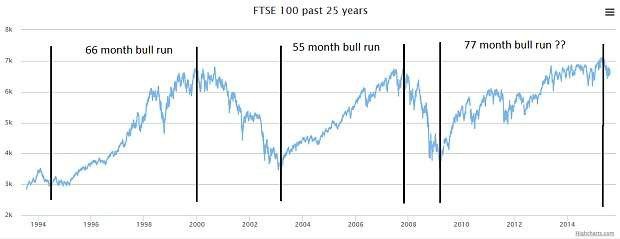

7 – Bull market third longest on record

The UK stock market is in its 77th month of a bull market, which began in March 2009. On only two other occasions in history has the market risen for longer. One is in the lead-up to the Great Crash in 1929 and the other before the bursting of the dotcom bubble in the early 2000s.

UK markets have been a beneficiary of the huge balance-sheet expansion in the US. US monetary base, a measure of notes and coins in circulation plus reserves held at the central bank, has more than quadrupled from around $800m to more than $4 trillion since 2008. The stock market has been a direct beneficiary of this money and will struggle now that QE3 has ended.

8 – Overvalued US market

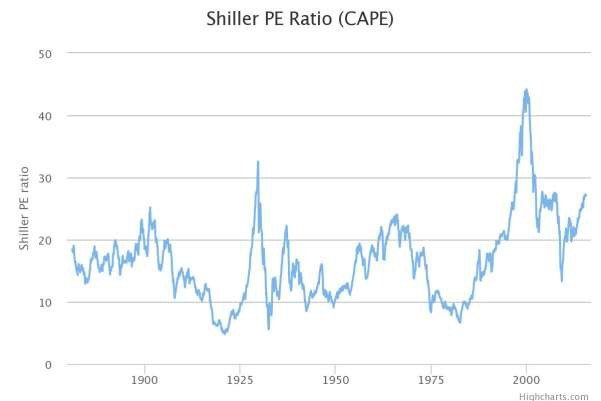

In the US, Professor Robert Shiller’s cyclically adjusted price earnings ratio – or Shiller CAPE – for the S&P 500 stands at 27.2, some 64pc above its historic average of 16.6. On only three occasions since 1882 has it been higher – in 1929, 2000 and 2007.

End of Telegraph article

Another article by David Stockman on 15 August 2015

The Great China Ponzi—An Economic And Financial Trainwreck Which Will Rattle The World – by David Stockman 16 August 2015

There is an economic and financial trainwreck rumbling through the world economy. Namely, the Great China Ponzi. In all of economic history there has never been anything like it. It is only a matter of time before it ends in a spectacular collapse, leaving the global financial bubble of the last two decades in shambles.

But here’s the Wall Street meme that is stupendously wrong and that engenders blind complacency with respect to the impending upheaval. To wit, the same folks who brought you the myth of the BRICs miracle would now have you believe that China is undergoing a difficult but doable transition——-from an economy driven by booming exports and monumental fixed asset investment to one based on steady as she goes US-style consumption and services.

There may well be some bumps and grinds along the way, we are cautioned, such as the recent stock market and currency turmoil. But do not be troubled—–the great locomotive of the world economy will come out the other side better and stronger. That’s because the wise, pragmatic and powerful leaders and economic managers who deftly guide China’s version of capitalism have the capacity to make it all happen.

No they don’t!

China is not a clone-in-the-making of America’s $18 trillion consume till you drop economy—-even if that model were stable and sustainable, which it is not. China is actually sui generis—–a historical freak accident that has no destination other than a crash landing.

It’s leaders are neither wise nor deft economic managers. In fact, they are a bunch of communist party political hacks who have an iron grip on state power because China is a crude dictatorship. But their grasp of the fundamentals of economic law and sound finance can not even be described as negligible; it’s non-existent.

Indeed, their reputation for savvy and successful economic management is an unadulterated Wall Street myth. The truth is, the 25 year growth boom in China is just a giant, credit-driven Ponzi. Any fool can run a central bank printing press until it glows white hot.

At the end of the day, that’s all the Beijing suzerains of red capitalism have actually done. They have not created any of the rudiments of viable capitalism. There are no honest financial markets, no genuinely solvent banks, no market driven allocation of capital and no financial discipline which comes from the right to fail as well as succeed.

There are, for instance, 287 million equity trading accounts in China, most of them opened within the last year and overwhelmingly held by retail punters with sub-high school educations. In less than 12 months they took down upwards of $1 trillion of margin debt through official brokerage channels and a massive network of shadow banking sources including dodgy peer-to-peer lending arrangements.

So fortified, they clambered after a stock market bubble that expanded by $3 trillion in just 60 trading days ending on June 14, and then broke into a panicked selling stampede that liquidated that very same $3 trillion of bottled air in hardly 20 trading days thereafter.

Then the state sent out the paddy wagons to arrest and intimidate the panicked sellers and threw-open the central bank’s credit lines to fund hundreds of billions of unwanted stocks. That is not capitalism, red or otherwise; it’s desperate, mindless madness.

Likewise, there are no credible institutions of contract law and bankruptcy. There is not even minimally honest corporate financial reporting and no restraints at all on the propensity of China’s newly affluent masses to gamble in real estate, stocks, commodity financing schemes, dodgy private lending clubs, chain letters and endless similar get rich quick schemes.

Most importantly, there are no lines of demarcation between the property of the state and the license of officialdom and their cronies to expropriate it. In a word, China wallows in the greatest cesspool of corruption known to history because that’s what happens when you erect a $10 trillion command economy virtually over night.

And the swaying edifice of red capitalism has indeed been stood up overnight. At the time that Mr. Deng radically changed the party line——proclaiming that it is glorious to be rich and the PBOC slashed the RMB exchange rate by 60% in 1994 in order to jump start an export boom——there was less than one half trillion dollars of credit market debt outstanding. Alas, that figure today is $28 trillion according the cautious reckoning of McKinsey, and most likely far more.

Here’s the thing. You can not safely, sanely or efficiently grow by 56X in hardly two decades something as combustible as cheap, come-and-get it state supplied credit in an environment where the rudiments of market capitalism do not even exist. If you pursue that kind of financial Frankenstein, that’s exactly what you will get, and that’s what the comrades in Beijing actually got.

Now, however, the iron law of financial bubbles has caught up with them. That is, when you stop supplying increasingly massive amounts of new credit to what eventually becomes an elephantine bubble, it begins to fall inward.

This happens slowly at first, then with accelerating momentum, and finally culminates in a panic-riven meltdown. That sequence encapsulates the entirety of the 2006-2008 securitized mortgage meltdown on Wall Street, the late 1980s and early 1990s Tokyo real estate boom and bust, the 1979-1980 silver and gold bubbles and countless others stretching back centuries in time.

So the passive-aggressive posture of China’s officialdom about what even they recognize as the out-of-control credit bubbles in their realm has no rhyme or reason. Beijing’s recent hopping from one foot to the other, first stimulating and then braking, is rooted in pure desperation and seat of the pants adhockery.

Wall Street sees none of this, however, and for a reason dripping with irony. Namely, since the ascension of Alan Greenspan to the Fed in 1987, the epicenter of world capitalism—— that is, the money and capital markets of Wall Street—-has fallen prey to a regime of monetary central planning. Price discovery in the financial auction markets has been supplanted by price administration decreed by the twelve mortals who comprise the FOMC. A monetary politburo, if you will.

Not only has this increasingly heavy-handed central bank intrusion falsified financial asset prices, subsidized rampant carry trade speculation, eliminated an honest risk-reward calculus and destroyed short sellers and other natural instrumentalities of financial discipline, but it has also drastically changed the culture of the financial markets.

The overwhelming share of players in what has become a central bank enabled casino are now de facto statists. They believe that the agencies of the state can and should peg money market interest rates, prop up the bond market via massive monetization of the public debt, and eliminate “contagion” outbreaks in the equity and other risk asset markets.

Except “contagion” is a red herring. Its just another name for old-fashioned market breaks and bear raids on speculative excesses and reckless leveraged gambling. This kind of bear market liquidation is essential for healthy capital and money markets, but its been extinguished by the Greenspan/Bernanke/Yellen “put” and the casino’s overwhelming

conviction that the central bank will flood the market with liquidity should another Lehman- style meltdown ever manage to incept.

All of this adds up to the conviction that governments drive the process of economic growth and wealth creation and that capitalism thrives best when it is nourished and guided by the helping hand of the state, most especially its central banking branch.

Needless to say, that self-serving but misbegotten ideology would never have taking root in Wall Street 50 years ago. In the days when the great William McChesney Martin took away the “punch bowl” just six months after the 1957-1958 recession ended by a series of stiff interest rate increases and by raising stock margin requirements to 90% of market value, the captains of finance would never have dreamed of 80 straight months of zero money market rates, as has now occurred.

They would have been screaming to high heaven that such radically unsound finance was a mortal danger to the nation’s wealth. By contrast, today they think they are entitled to central bank “accommodation” for as long as might be necessary to keep the stock averages rising. So while 80 months of ZIRP is nothing less than a recipe for massive speculation that will inexorably lead to a resounding bust they don’t even notice the danger.

Worse, the Wall Street casino inhabitants have no clue that while bubble finance is dangerous enough in a relatively mature capitalist economy like that of the US, it is pure monetary nitroglycerin in a setting like the China credit Ponzi.

Nor do they have the slightest inkling that PBOC head, Zhou Xiaochuan, is not just an Asian version of Janet Yellen who wears trousers and dyes his hair black.

Stated differently, Wall Street cannot see straight when it comes to China because its crypto- Keynesian lenses lead it to suppose Mr. Zhou will stump up whatever liquidity and bailouts may be necessary and that his colleagues in Beijing will open the fiscal stimulus spigots if growth continues to falter.

Well, Mr. Zhou may talk the idiom of central banking, but he’s just a servant of the communist party overlords whose overwhelming purpose is to stay in power and whose colossal economic and financial ignorance will lead them to destructive expedients. What lies ahead will make the paddy wagon brigades now combing the brokerage houses look mild by comparison.

Its too late for a soft landing and managed deflation of the Great China Ponzi. That’s because in their heedless resort to the printing press and credit driven expansion over and over during the past two decades they have generated “freakish impossibilities” throughout the length and breadth of the Chinese economy.

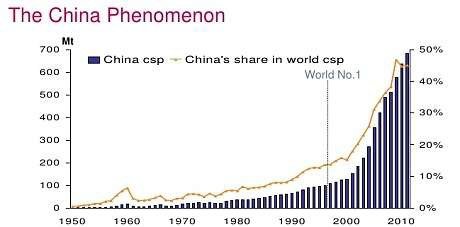

For instance, the Chinese steel industry grew by 11X during the last 20 years, expanding from 125 million tons, which was already larger than the US and Japanese steel industries in the mid-1990s, to 1.1 billion tons today. But neither China nor the world can use that much steel, even as China’s aggressive “dumping” on the world market gathers force.

China’s steel output.

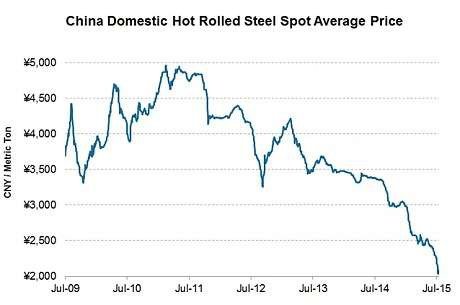

In fact, China’s steel production is already swooning—–with output in the most recent month down nearly 5% Y/Y and prices off 26% since January and 55% since the three-year ago peak. During the first half of 2015, China’s large and medium steel mills spewed $3.5 billion of red ink, and that just a warm up for the carnage yet to come.

In a word, China has upwards of 400- 500 million tons of steel capacity that will be idle once its construction boom stops and the rest of the world throws barriers up against its exports.

That amounts to economically destructive malinvestment on an unprecedented scale. The idling of China’s giant steel mills, in turn, will create an economic void which will cause a massive collapse of business, employment and incomes up and down the iron and steel food chain.

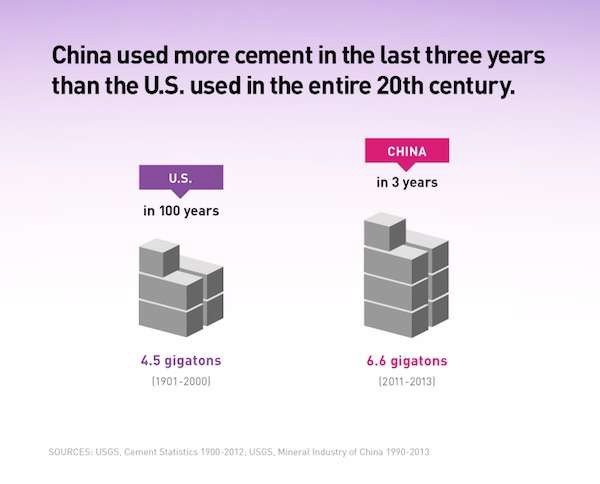

Likewise, China’s construction infrastructure is grotesquely overbuilt from cement kilns, to construction equipment manufacturers and distributors, to sand and gravel movers, to construction site vendors of every stripe. For crying out loud, in three recent year China used more cement than did the United States during the entire 20th century!

That is not indicative of a just a giddy boom; its evidence of a system that has gone mad digging, hauling, staging and building because there was unlimited credit available to finance the outpouring of China’s runaway construction machine.

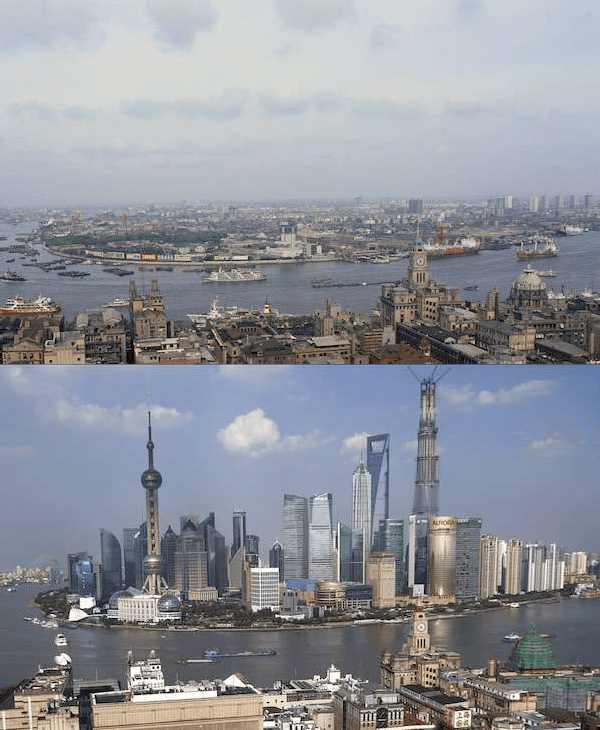

To get a feel for this outbreak of collective insanity, look at Shanghai’s f inancial district in 1987 and again in 2013:

The setting is Shanghai’s financial district of Pudong, dominated by the Oriental Pearl Tower at left, and the new 125-story Shanghai Tower, China’s tallest building and the world’s second tallest skyscraper, at 632 meters (2,073 ft) high, scheduled to finish by the end of 2014. Shanghai, the largest city by population in the world, has been growing at a rate of about 10% a year the past 20 years, and now is home to 23.5 million people — nearly double what it was back in 1987.

Or take a gander at China’s ghost cities, fully equipped with everything, except people. This is merely an example of the stunning economic waste which covers the Chinese landscape:

In short, China’s freakish economy is just one great collection of impossibilities that cannot be stabilized or propped-up much longer. But in their desperation to forestall the inevitable crash, the suzerains of red capitalism will increasingly turn to the mailed fist of state repression.

Indeed, they can’t any longer rely on the proposition that party power comes from the end of Mr. Deng’s printing press. To pile on even more mountains of credit will only exacerbate the massive capital flight that is already underway and which threatens a devastating further plunge of the RMB exchange rate.

The latter is the Achilles Heel of the whole Ponzi. To arrest capital flight Beijing will have to do the opposite of what it has done for the last 20 years. That is, it will have to shrink the domestic money supply and banking system in order to sell dollars and euros rather expand domestic credit in order to sequester dollar liabilities (i.e. treasury bonds) at the PBOC.

In due course, China will be aflame with campaigns against corruption and “enemies of the state” as it seeks to cope with its collapsing financial bubbles and endless herds of economic white elephants. Chairman Mao’s axiom as to where state power really comes from——that is, the barrel of a gun—-will become the increasingly evident modus operandi of the communist party rulers.

The resulting deflationary spiral will suck the global economy into its vortex. And Wall Street will go down for the count because this time the Fed will be utterly powerless to reverse the tide.